Toss - Fintech’s Final Form, The Everything App

Through the turn of the century, few countries could match South Korea’s technological infrastructure. Internet speeds were the fastest in the world. Smartphones were ubiquitous. Digital adoption outpaced nearly every peer economy. Yet for all that sophistication, one basic function remained strangely broken: sending money. To transfer $20 to a friend, you had to download a separate security program, navigate a legacy bank website, obtain a government-issued digital certificate, manually enter a full account number, and pay a nontrivial per transaction fee. In a country where the average person holds more than 7 bank accounts, even the basic act of managing one’s own finances was slow, fragmented, expensive, and painfully complex.

In 2011, Seunggun “SG” Lee stood in his dental clinic at Samsung Medical Center in Seoul and knew something felt wrong. On paper, he had it all: elite training, a thriving career, the prestige of one of the country’s top medical centers. But SG felt constrained and unfulfilled by his future career path. “People fear failure in Korea because failures are rarely forgiven,” SG later reflected. “I had security against failure, but I wasn’t happy because I wanted to create more impact at scale.”

Outside of the Medical Center, Samsung was transforming the mobile ecosystem and propelling Korea to the forefront of the global smartphone revolution. After seeing Steve Jobs continue to change the world with the Apple iPhone, SG was inspired and wanted to be a part of the digital shift. He eventually quit his job, and after 8 failed product ideas, SG launched Toss in 2015: a simple app that lets Koreans send money without hassle. In just a decade, Toss has grown to become the financial control center for ~30 million South Koreans, reaching nearly 60% of the country’s population. We at Meritech are thrilled to announce our investment in Toss.

Moving Money But Not Making Money

At Meritech, we first met SG on a trip he took to the US in 2016, about 18 months after Toss launched. The business had exceptional viral user adoption (growing 10x Y/Y) with over 4M downloads, close to 20x Y/Y payment-volume growth, and remarkably strong retention. Toss’s product was transformative, it was simple, beautiful, and free. It enabled Koreans to easily move money from one bank account to another with a recipient’s phone number, a few taps and at no cost.

However, there was a very big problem…Toss was heavily subsidizing that expensive bank-to-bank transfer fee on behalf of their users. For years, Toss had a negative gross margin, and the faster their network grew, the more money Toss lost! As losses mounted, many feared that the core product users loved was functioning on an unsustainable cost structure. Questions loomed: How long would investors fund Toss to subsidize their core product? Would users continue to trust Toss with their money? How would Toss eventually make money?

Money Movement to Korea’s Money App

Despite the questions, SG remained obsessively focused on consumer experience and Toss’s core mission, removing friction from money. As consumer adoption and love spread through Korea, Toss forced Korea’s top financial regulator, the Financial Services Commission (FSC), to confront how outdated the country’s financial and data infrastructure had become.

In 2019, the FSC launched the Open Banking initiative. This required all banks to open up their customer data and payment rails to third-party fintech companies through standardized APIs. Notably, this regulation enabled both read and write access for stakeholders, unlike the U.S. system which only allows data aggregation; fintech companies could now initiate payments and query balances from any bank. Toss was among the first to connect to the new banking system, and it was transformative. Users could connect every bank account they owned – the average Toss user now links 16 different accounts – and move money between them instantly, for free, without ever leaving the app. Transfer volumes exploded under the new initiative.

Then, in 2022, the FSC launched MyData, establishing a nationwide open-finance and open-data framework that gives every individual the right to share their personal financial data with any licensed provider they choose. Toss secured an early MyData license. For users, it meant they could not only see all their financial information in one app, but orchestrate money across their life in Toss. For Toss, it unlocked the ability to deliver personalized insights and recommendations based on a complete picture of each user’s finances: budgeting, spend analysis, credit score tracking, and tailored advice.

Toss suddenly had something no U.S. fintech could dream of, a regulatory environment that required interoperability by design. Open Banking and MyData became critical pillars to Toss becoming a single control plane for money in Korea. But, what does that really mean?

If the U.S. Had Toss

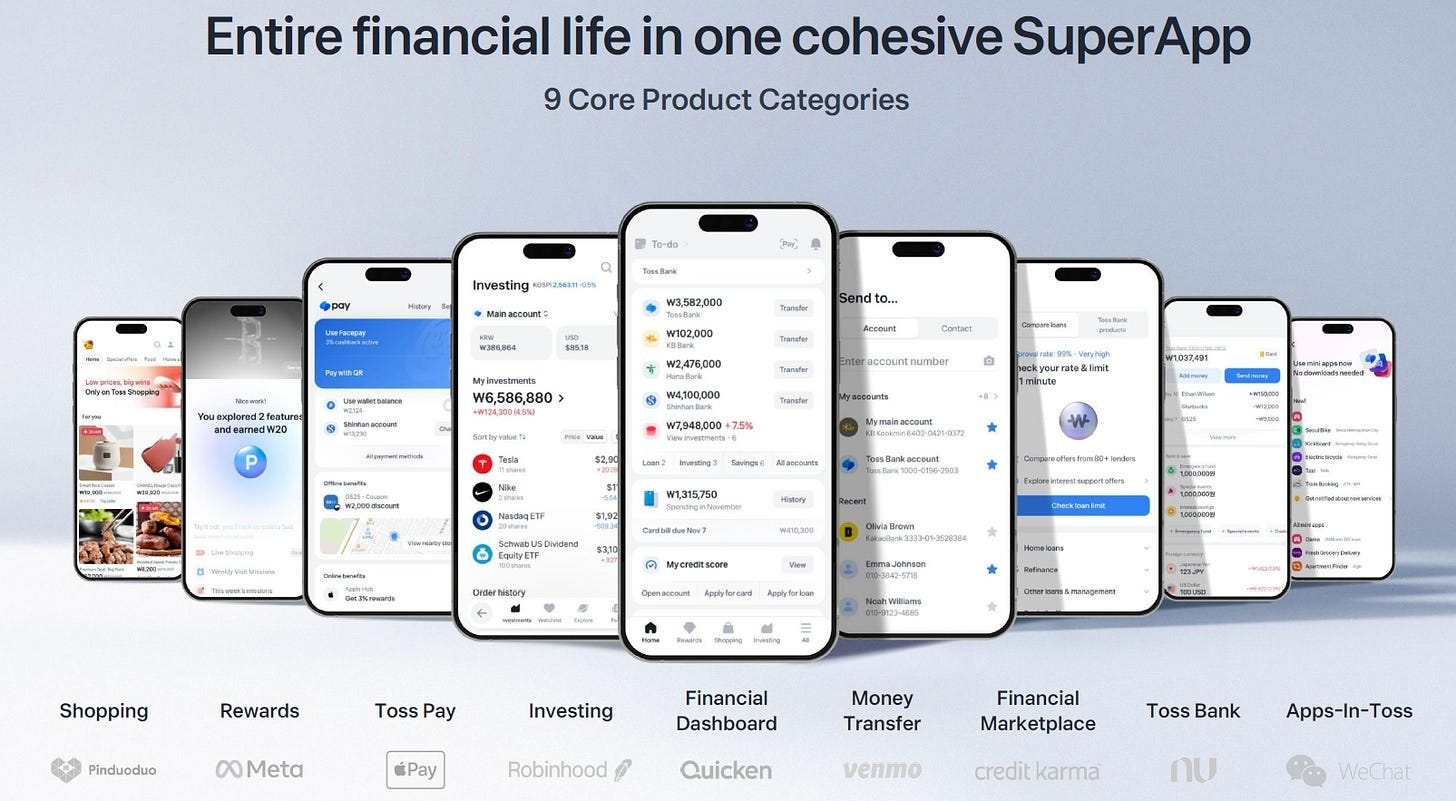

It is hard for westerners to grasp Toss because there is nothing like it in these geos. To better understand Toss, imagine your entire financial universe – your banks, credit cards, brokerage accounts, insurance policies, loans, merchant payments, rewards, bills, investments – living inside one beautifully simple mobile app. Not linked by Plaid, not manually synced, but a single app to fully orchestrate money, in real time, with open read-and-write access to every financial institution in the country!

It is as if JP Morgan, Bank of America, Capital One, TurboTax, Credit Karma, Robinhood, LendingTree, SoFi, Stripe, Square, and PayPal merged into one and were redesigned from scratch with an obsessive focus on a single coordinated user experience. Users never need to take any action outside of Toss. Imagine never logging into any of your bank accounts, credit cards, brokerages, lenders, tax software, or payments apps ever again. Imagine applying for any new financial product within that single super app, because you have the equivalent of a financial passport that can efficiently apply for financial products with the tap of a button. Imagine hundreds of thousands of merchants accepting payments from that app directly via Toss Pay using just facial recognition (Face Pay).

But Toss didn’t stop, they have kept extending their app beyond fintech into areas like ecommerce (Amazon), ride-hailing (Uber), mobile phone service (Verizon), and its own app marketplace (App Store). Toss has become the everything app. It is hard to imagine how all of this functionality can live in a single app, but that is Toss today. How is this all possible?

The Money App to Making Money – Rewiring Consumer Finance

Even prior to the regulatory tailwinds of Open Banking and MyData, Toss’s monetization model was more of a first principle than a strategy. Unlike closed financial service providers who monetize through traditional revenue levers like fees, interest, interchange, and net-interest margin, SG saw it differently, “Our long-term vision is not another financial holding company, but a global internet company built on financial services.” Toss isn’t a bank, it is a network, more analogous to Facebook than to any financial institution. It just happens that the core engagement mechanism for Toss is money, whereas for Facebook, it is social networking and entertainment.

Rather than charging consumers, Toss began building products that let businesses access its highly engaged user base. Banks and financial institutions can distribute loans, insurance, and deposit products directly through Toss. Advertisers can use MyData to deliver hyper-targeted, high-intent ads. Businesses can accept Toss payments for a small fee. Ecommerce merchants can sell inside Toss’s ecosystem.

The brilliance of this model is that it simultaneously accelerates product velocity, speed to market, enables massive scale, lowers operating costs, and delivers a meaningfully better consumer experience. Furthermore, in the case where Toss feels like they have a competitive edge in a specific financial product - like banking with Toss Bank, which Toss is the largest shareholder with 28% ownership - they are bold enough to develop their own products and let the offering compete directly against the rest of the market.

Let’s take personal loans as an example. If Toss wanted to build its own loan book, it would inherit the full operational weight of a traditional lender including underwriting, capital markets, servicing, collections, and regulatory oversight, all of which are slow, expensive, and difficult to scale. Consumers would only see the loans Toss could offer, even if another provider has a better rate.

Instead, Toss runs a loan marketplace. Its clean, unified UI abstracts away the friction and presents consumers with all available offers in one place, instantly. The best offer wins, consumers get more competitive pricing, and Toss avoids the burden of building and scaling a full-stack lending operation.

This model doesn’t just improve a single product line, it rewires the economics and product velocity of the entire business. By removing the need to build and scale full-stack financial infrastructure, Toss can test, launch, and scale new products at a pace traditional institutions simply cannot match.

This is another compounding network effect of the Toss ecosystem, and the proof is in the app’s engagement. 1 in 5 Koreans goes on Toss every day, and checks the app more than 11 times per day. They’re actively using over 3.5 products across the 9 core products of the super app. The marketplace architecture accelerates adoption and engagement. Every new product slot becomes a competitive arena where the best provider wins, the consumer benefits, and Toss expands its role as the default financial ecosystem for tens of millions of Koreans. This all aligns with SG’s vision on being a founder, “I believe entrepreneurship comes from a desire to provide a social contribution, beyond simply making money. Toss’s mission is to provide the best possible financial service experience to users.”

The Longest Sale Cycle In Meritech History – Investing in Toss

Almost nine years after first meeting SG, Meritech is investing in Toss. It is simple, we believe that Toss has the structural advantages to create one of the most successful and enduring global internet franchises:

The world’s deepest financial data network powered by dominant user penetration and unprecedented engagement

An ambitious culture that is relentlessly focused on product velocity and innovation

World class talent density and leadership

Toss continues redefining the art of what is possible, something only the most special founders and companies can. At Meritech, we aim to partner with Market Leaders in the Markets that Matter and take a very long-term view. We’re confident SG will keep making people smile, not with a toothbrush, but by relentlessly innovating and building everything that users need. We couldn’t be more excited to partner with SG and the Toss team.

| A guest post by

|

| A guest post by

|