2025 Technology Exits in Review

A review of the 2025 technology exit environment

As 2025 has come to a close, we did a review of technology IPOs (initial public offerings) and M&A (mergers and acquisitions) in 2025.

2025 was slated to be a massive year with the IPO window “blown open” by some accounts. Though we saw an acceleration in IPOs at the end of 2025, in reality, it barely cracked open. In 2025, there were only 6 pure-play software/infrastructure IPOs and 7, if you include CoreWeave, an AI infrastructure company. For context, in 2021, there were 27 pure-play SaaS IPOs (16 in 2020).

IPOs are also not the only path for exit, as M&A came roaring back with a total of $587B in volume across both public and private technology companies, the largest volume in the past decade.

2025 Venture-backed IPOs

In 2025, several factors contributed to a subpar IPO year, including the market’s tariff shock in the spring and the government shutdown in the fall; however, the larger reality is that the public markets have been less appealing to the most promising companies that were public-company ready in 2025. The era of multi-hundred-billion-dollar private companies continues (and soon to be trillion+) with companies such as SpaceX, OpenAI, Anthropic, Stripe, Databricks, and others opting to raise private capital in 2025 despite significant demand for their shares in public markets. Given the abundance of private market capital and the expediency/ease of remaining private, it is unclear whether we will see a tidal wave of IPOs in 2026, as was also expected in 2025, or fewer with larger volumes (if companies such as SpaceX or Anthropic go out).

The following provides a deeper analysis of the 2025 cohort.

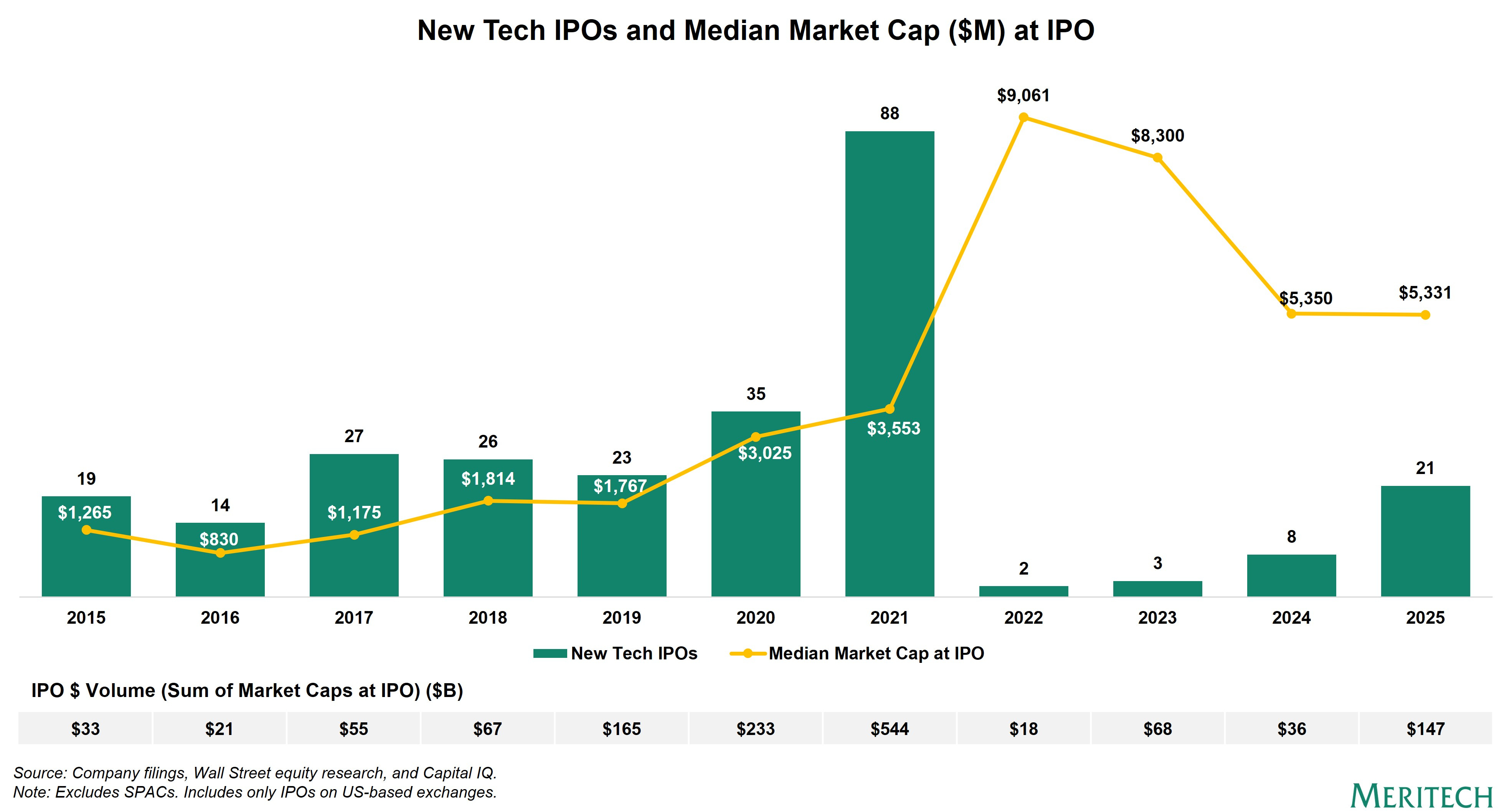

2015 —> 2025 U.S. Tech IPOs, Median Market Capitalization, and Total Volume

The chart below shows U.S. tech IPOs over the last 10 years. While 2025 was a significant improvement over 2024, we’re only even close to the ZIRP (zero-interest-rate-policy) era for the number of IPOs. That said, the median market cap at IPO is rising as outcomes are larger as companies are staying private longer.

2025 Software / Infrastructure IPOs

What did the software IPOs in 2025 look like? The following list includes software/infrastructure IPOs in 2025, sorted by IPO market capitalization. Apart from Gloo, a small-cap company, all priced in the billions in market capitalization.

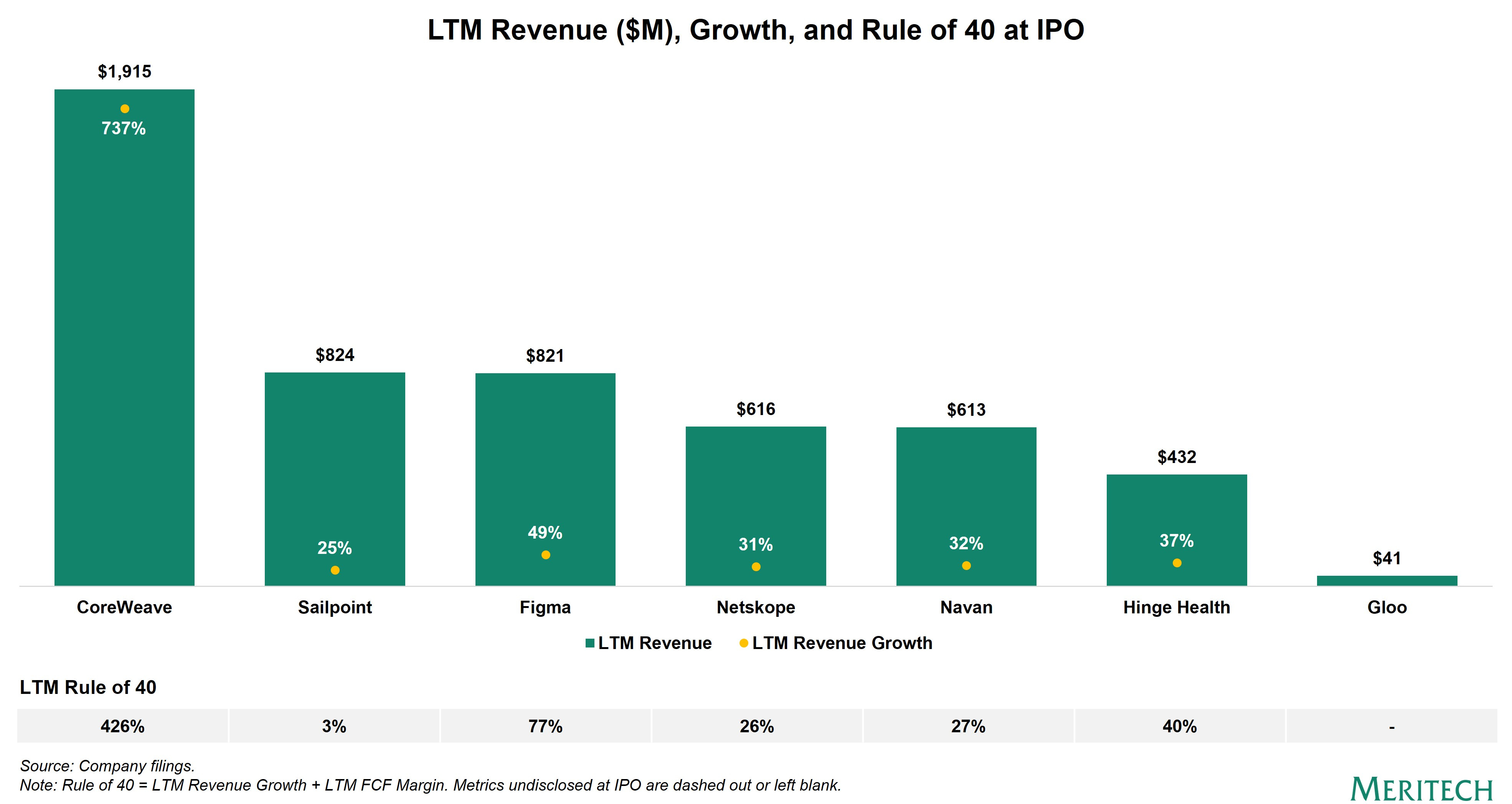

LTM (Last-twelve-months) Revenue & Growth and Rule of 40

Here is a view of LTM revenue, revenue growth and Rule of 40. As you can see, CoreWeave stands out given their astronomical revenue growth rate and scale. Figma was a standout too, with almost 50% year-over-year revenue growth and almost 30% free cash flow margin on over $800M of LTM (last-twelve-months) revenue and ~$1B of implied ARR. The median LTM revenue is $616M with 35% LTM revenue growth and (5%) LTM free cash flow margins.

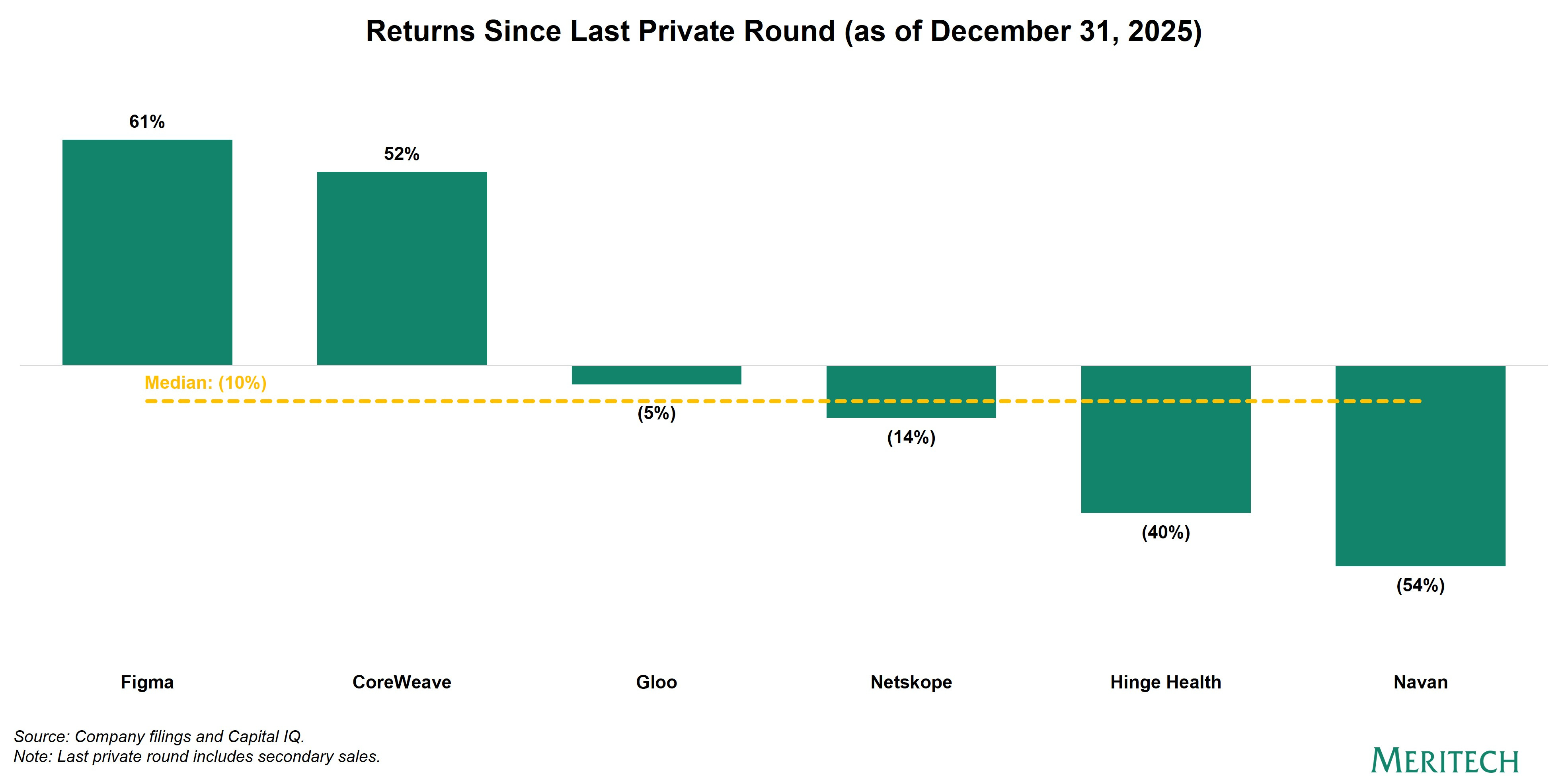

Returns from Last Reported Private Round

Interestingly, returns from the most recent private rounds have been muted, with the exception of Figma and CoreWeave, which are up 61% and 52% as of the end of last year, respectively. The median is (10)% from this group.

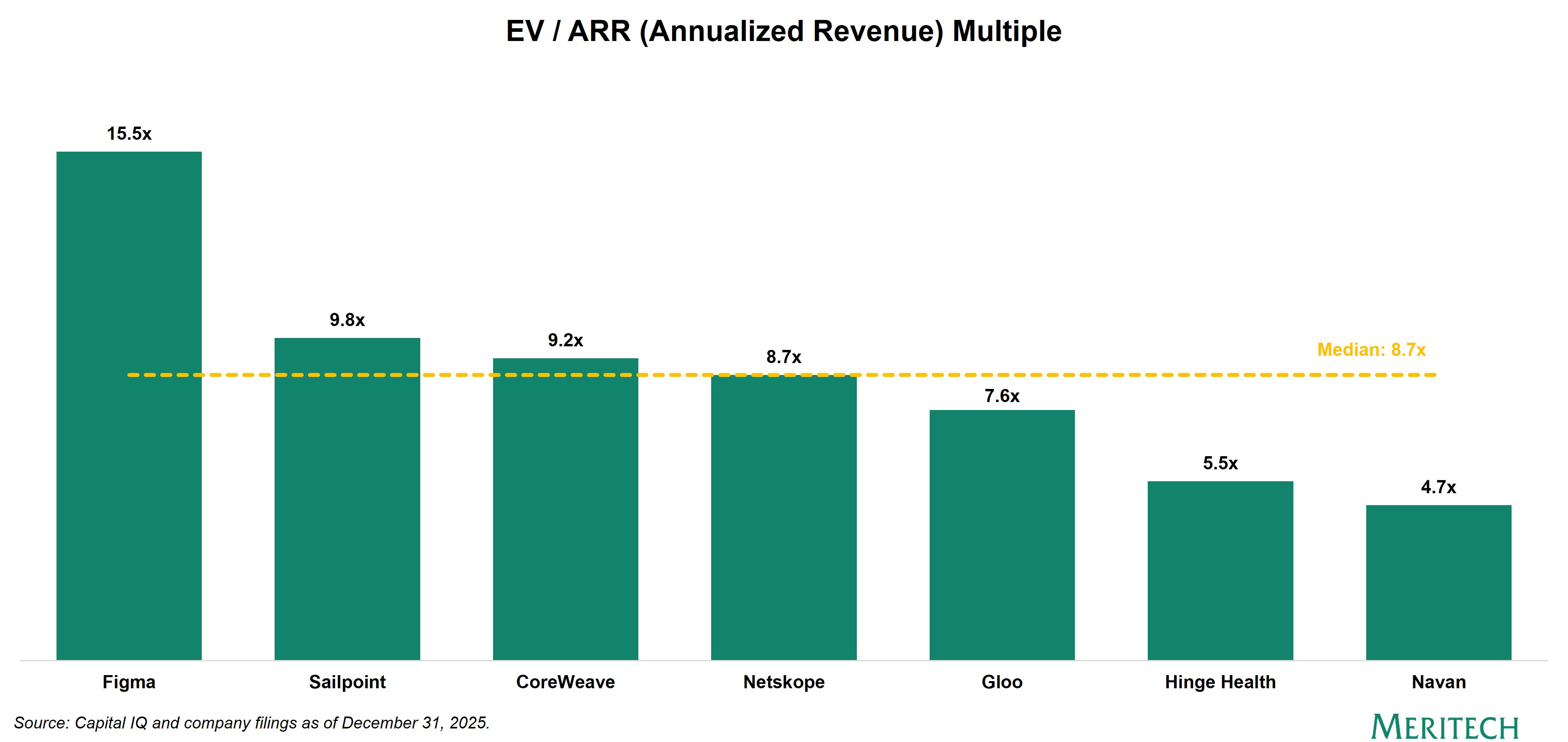

Valuation: Enterprise Value / ARR (Annualized Revenue)

Where are these companies trading today in regard to valuation? The following chart looks at EV / ARR (Annualized Revenue). Figma is the only company trading above 10x EV / ARR and the median is 8.7x.

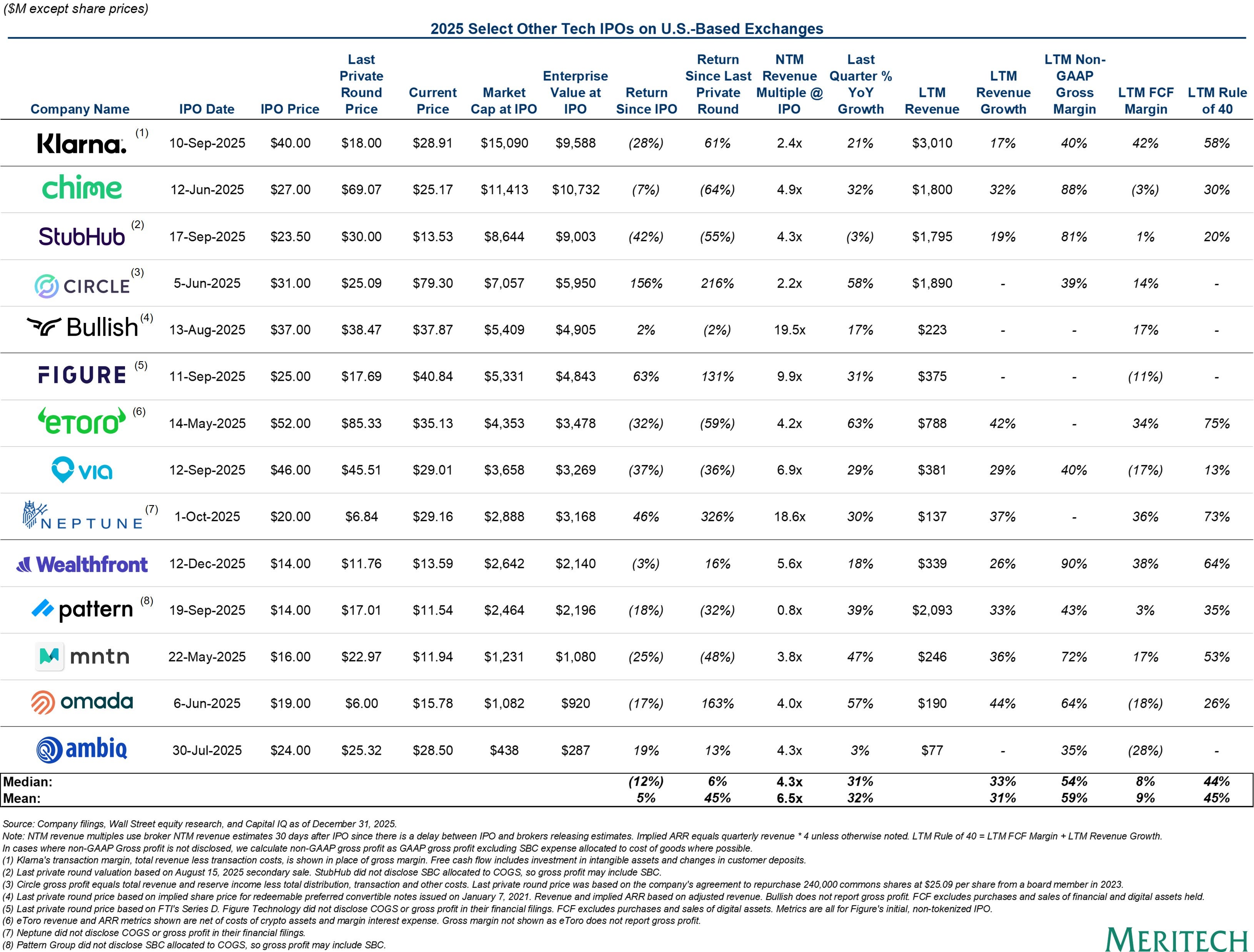

2025 Non-Software / Infrastructure Technology IPOs

While the above looked at pure-play software and infrastructure companies, the following looks at select non-software/infrastructure technology IPOs across consumer, fintech/crypto, and healthcare, sorted by market capitalization.

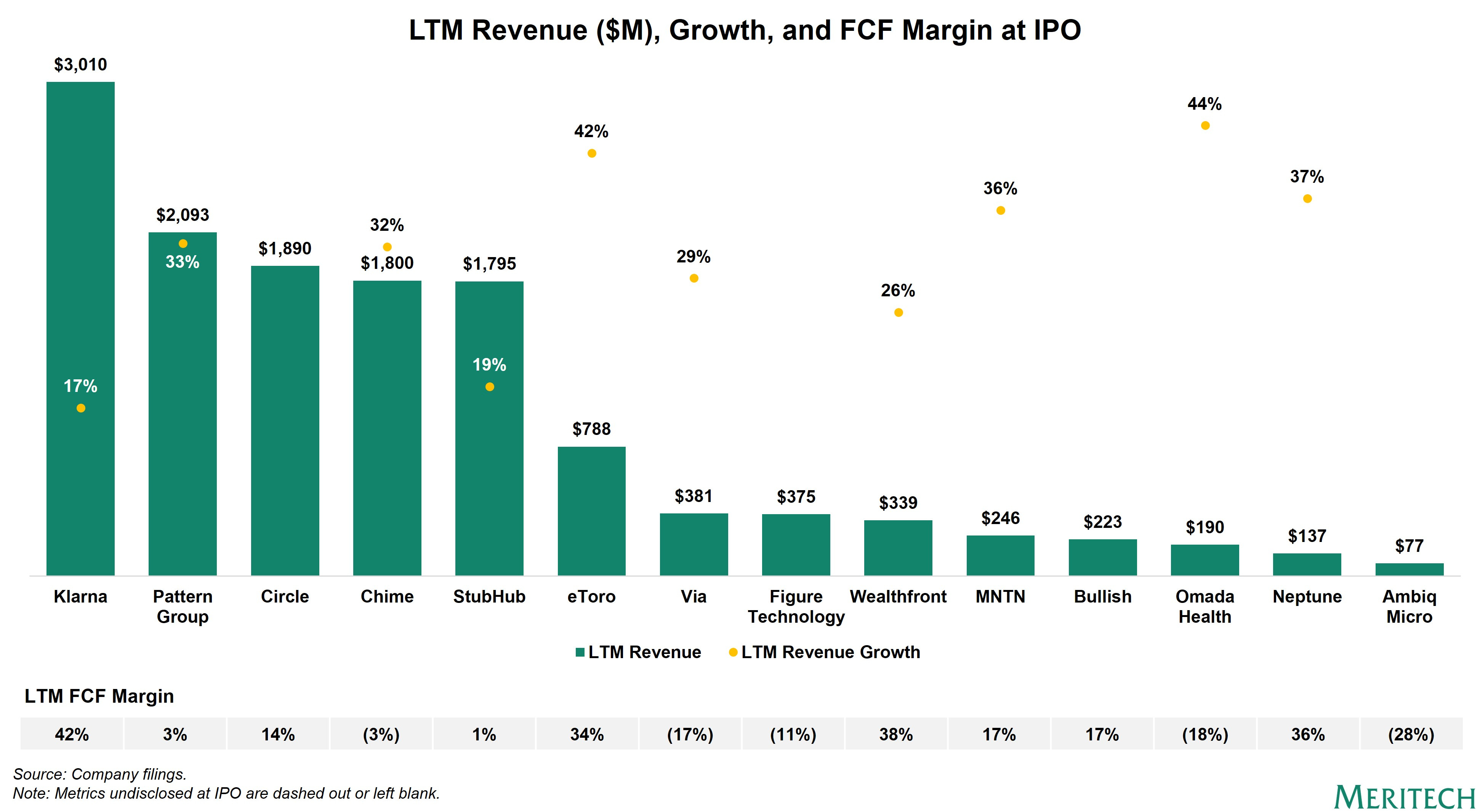

LTM Revenue & Growth and Free Cash Flow Margins

Given the spectrum of business models and companies, the revenue scale, growth, and margins of these IPOs vary more widely than those IPOs in software/infrastructure. The median LTM revenue is $378M with 33% LTM revenue growth and 8% LTM free cash flow margins.

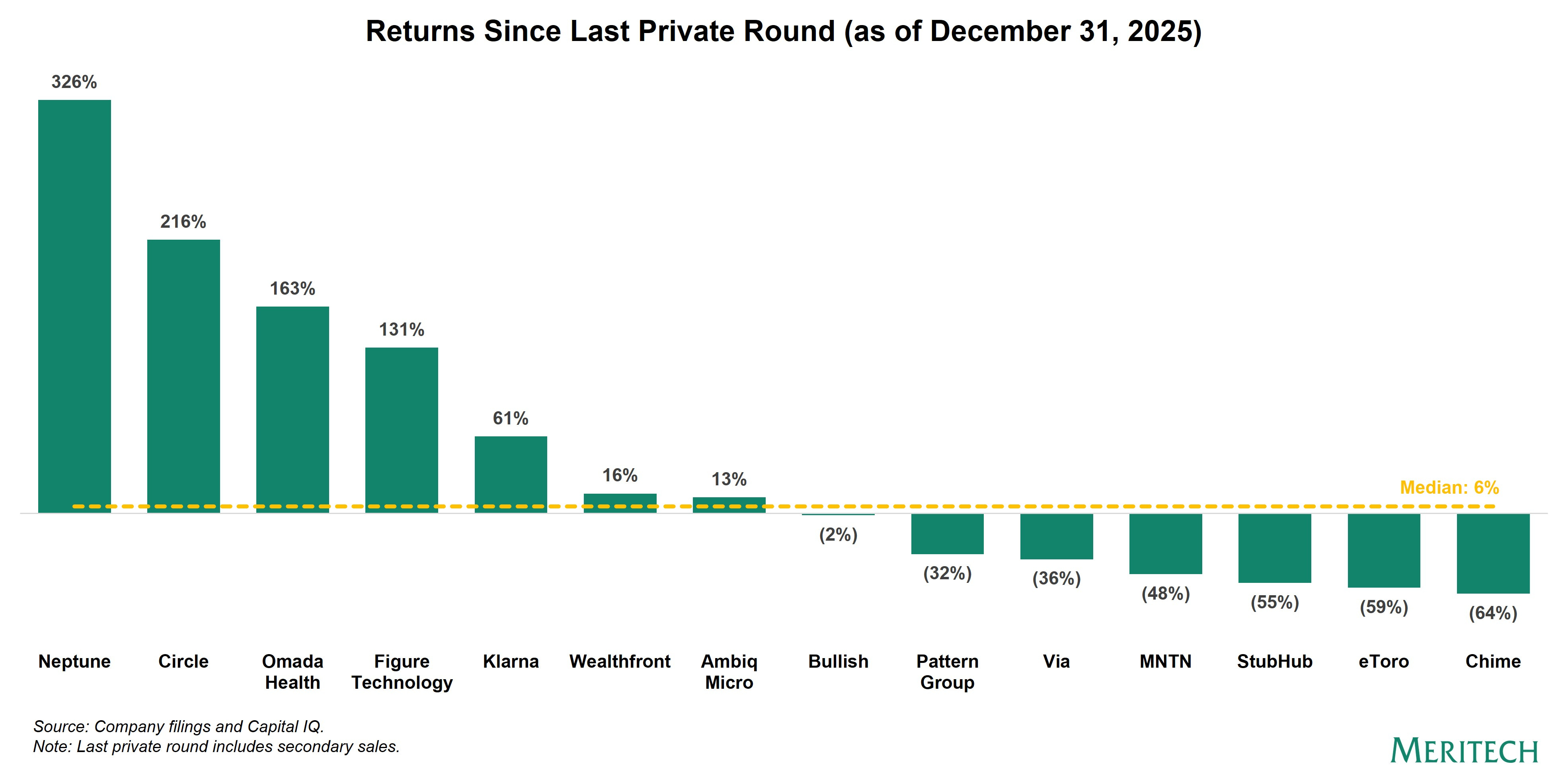

Returns from Last Reported Private Round

The returns from their last private round —> today are also disparate, but there are a few trading significantly above their last private rounds. The median across all is a 6% return.

Overall, there were 21 technology IPOs in 2025, with a total IPO market capitalization of nearly $150B. The top 5 companies by market capitalization – CoreWeave, Figma, Klarna, Sailpoint, and Chime – account for 56% of the total. While expectations were high in 2025, they’re even higher in 2026 with companies such as SpaceX reportedly considering what would be the largest IPO ever. Moreover, Anthropic was reported to be prepping for an IPO and also just did another financing. There is also a longer list of other large, fast-growing businesses, such as Databricks, Stripe, Canva, Revolut, and others that may choose the public markets. Time will tell whether they tap public markets or continue to raise private primary and secondary capital.

2025 Private and Public Technology M&A

While the IPO market for venture-backed technology returned to 2019 or pre-ZIRP levels, the M&A environment in 2025 was extremely robust, and 2025 was the highest year for M&A transactions over $50M in the past decade. We believe a huge driver was the perceived change in the regulatory regime, particularly in the U.S., and this should continue into 2026.

Global Tech M&A Volume by Year >$50M ($B)

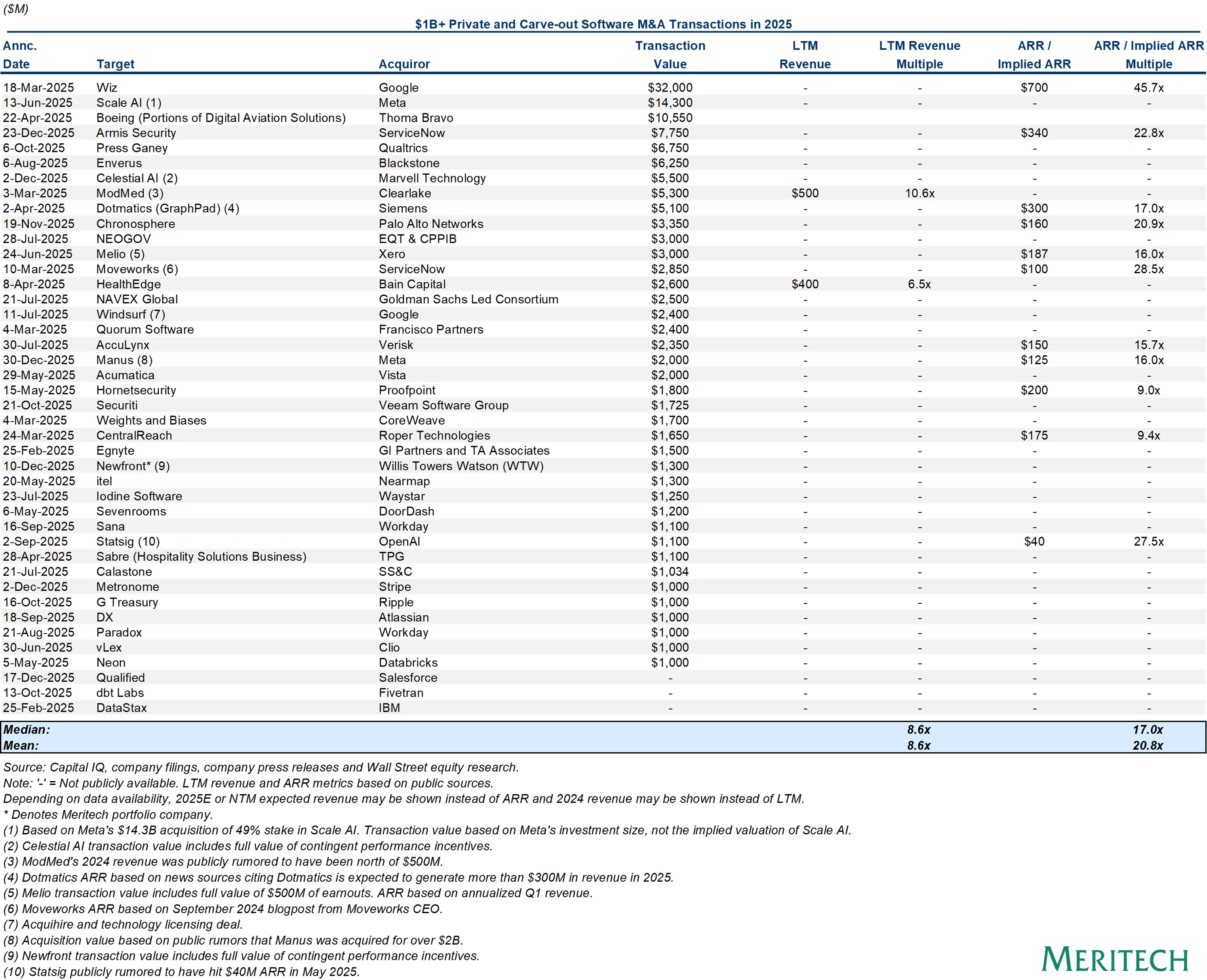

2025 $1B+ Private Software/Infrastructure M&A and Carve-outs

The following table shows private software/infrastructure M&A in 2025, sorted by transaction value. There were 3 venture-backed companies acquired for more than $5B: Wiz ($32B), Scale AI ($14.3B minority investment/dividend), and Armis ($7.75B). Because these are private companies, most do not report revenue or ARR figures, but we have included what was available in press releases and other public materials.

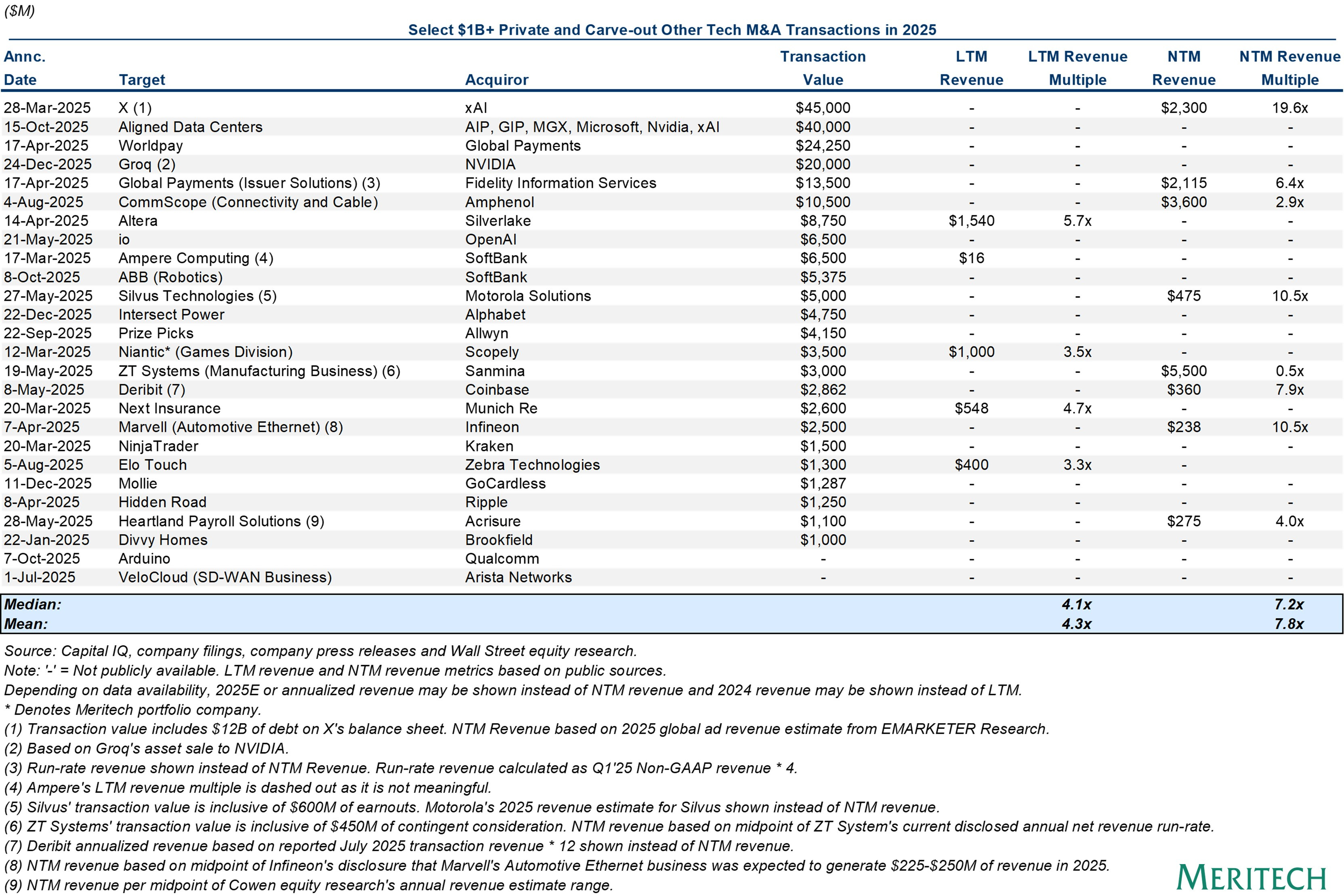

2025 $1B+ Private Non-Software M&A and Carve-outs

While the above table was limited to software, the following looks at non-software/infrastructure. Overall, although fewer in number, the top of this list comprises larger transactions, with a notable example being the Nvidia/Groq licensing deal announced on Christmas Eve 2025.

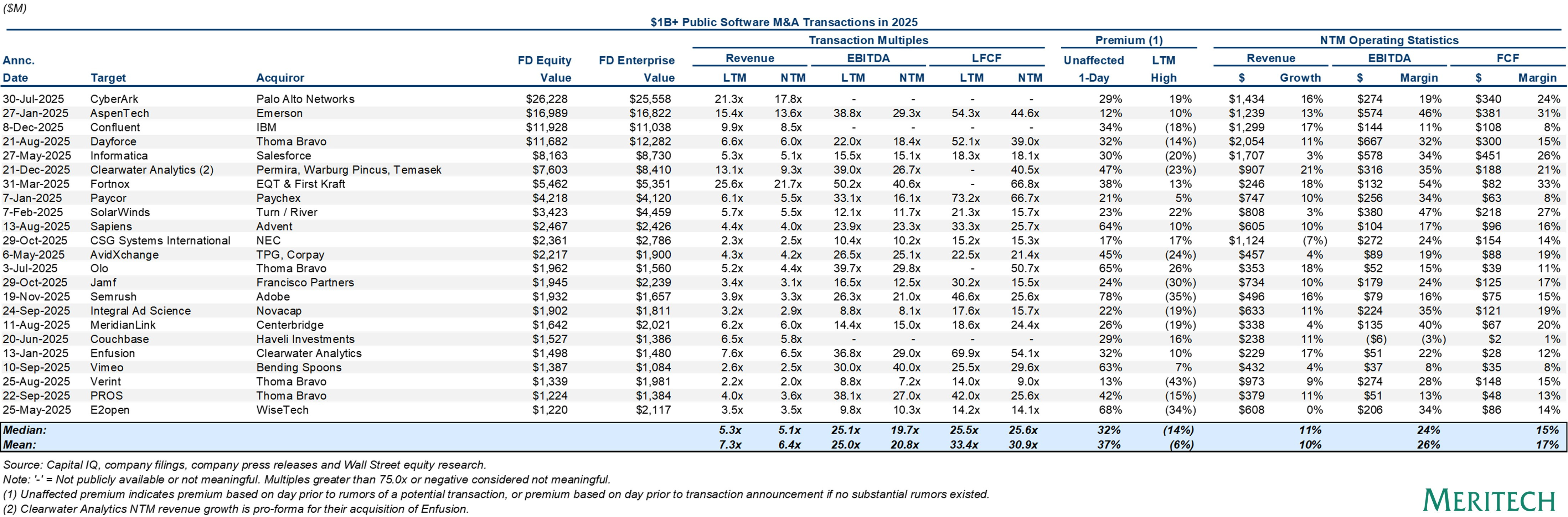

2025 $1B+ Public Software M&A

Now onto public software transactions over $1B. Interestingly, with the exception of a few companies, most multiples paid were <10x NTM revenue. Despite the fact that there are 92 public software companies trading below 10x NTM (next-twelve-months) revenue, or 85% of the total companies in our public software dataset, private equity (and strategics) have been less active. Certainly, the fear around non-AI stories is a contributor. It will be interesting to see if this trend continues in 2025. Across all companies we track, 60 trade below 5x NTM revenue, with a median NTM (next-twelve-months) revenue growth rate of 11%. While their valuations are reasonable for acquirers, their revenue growth rates are less compelling. Our full data set is here on Meritech Analytics.

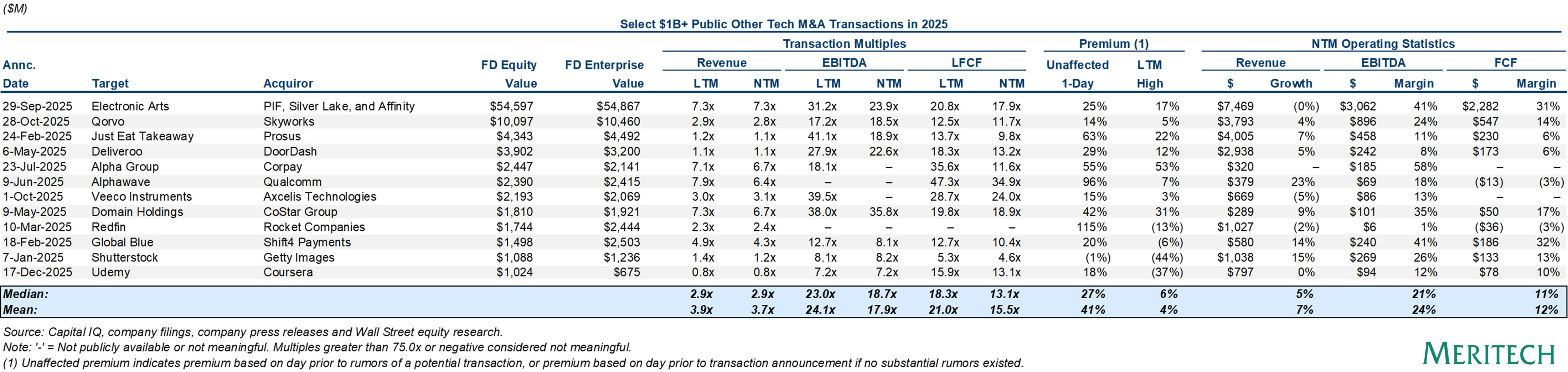

2025 $1B+ Public Tech Non-Software/Infrastructure M&A

In our final output, we included public non-software/infrastructure M&A for 2025. Apart from two larger transactions, most were <$5B in equity value.

Final Thoughts

2025 left more to be desired on the IPO front, but M&A was a bright spot with the highest volume in a decade. We are already seeing signs of a big 2026 with two companies filing their S-1s late last year, EquipmentShare and Motive, and it was just reported that Discord, a venture-backed communications platform, filed their S-1 confidentially. M&A is also off to a fast start with Hg announcing a $6.4B deal to take OneStream ($OS) private. If we had to predict, 2026 should be a strong year for liquidity (market conditions notwithstanding) – we might have the largest IPO ever in SpaceX and a very exciting environment for M&A, particularly in AI.